Structured settlements are commonly associated with the payment of personal injury damages because of their advantageous tax-free treatment. But some business purchases and buyouts can also benefit from structured settlements using annuity payments from an insurance company.

While payments from these non-personal injury cases aren’t tax-exempt, the recipient (the seller of the business) only owes taxes on the amount of money received each year.

Financing Alternatives

To illustrate when structured settlements might work, suppose a buyer of a private business is unable to obtain financing from a bank. One option to finance the deal is an installment sale where the buyer puts up a percentage of the purchase price and the seller receives a promissory note for the balance. Payments are to be made monthly or quarterly.

The seller may be concerned about default. The loan may be secured by company stock or assets and involves a personal guarantee. But the seller must ultimately rely on the buyer’s ability to make the payments.

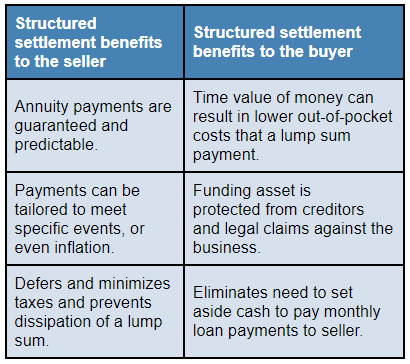

Another less risky option may be a structured settlement. Here, the buyer purchases an annuity from an insurance company, which makes monthly payments to the seller. The transaction reduces the seller’s risk of not getting paid because the payments are secured by the annuity. Plus, the tax consequences are likely to be more favorable than a 100% cash sale. However, this technique only works if the buyer has the cash to purchase the annuity.

Another factor to consider in deciding whether to choose a structured settlement over a lump sum distribution is that a structured settlement — by its terms — only gives the recipient a right to receive money in accordance with the schedule set out in the settlement document. It doesn’t give the recipient or the payer any ownership interest in the funding asset, thus preventing creditors of either party from levying upon the structured settlement funds.

Time Value of Money

Cost savings can also make the use of structured settlements attractive. Because the underlying annuity or government obligation is purchased with today’s dollars, the out-of-pocket cost is less than the total amount of money that the structured settlement will pay out over time.

Of course, with any structured settlement offer, it’s important to know the present value of the future payments. This allows the parties to compare the offer with an immediate cash payment.

Also, the present cost of a structured settlement depends on the amount of the future payments and their timing. So it’s advisable to have an expert review the documentation and crunch the numbers.

For More Information

Annuity payments are only one way to finance the sale of a closely held company, professional practice, or partnership interest.

Contact Dan Keefer via our online contact form to learn how CBM can provide business valuation services to help structure a sale or merger that generates the best after-tax financial return.

© 2023

Councilor, Buchanan & Mitchell (CBM) is a professional services firm delivering tax, accounting and business advisory expertise throughout the Mid-Atlantic region from offices in Bethesda, MD and Washington, DC.